I came across this on You-tube:

http://www.youtube.com/watch?v=t29fgA5M7VA

This comes from the film Koyaanisqatsi (a Hopi word meaning life out of balance). From roughly minute 3 to minute 6 of this clip are shots of the notorious St. Louis public housing project Pruitt-Igoe, a subsidized housing project that was so awful, it was never more than 60 percent occupied. The eleven building complex of nearly 3000 units was torn down before it was 20 years old.

In a terrific essay ( http://www.soc.iastate.edu/sapp/PruittIgoe.html), Alexander Von Hoffman argues that even a well-designed Pruitt-Igoe would have been a failure, because St. Louis had been (and in fact continues to be) a dieing city. And so it has; the 4th largest city in the country in 1890 is now not among the top 50.

But Pruitt-Igoe was a representation of the modernist movement at its worst. The buildings were faceless and difficult to cool. Public spaces were neglected and shadowy, and bred crime. The shame is that the complex gave high-rise living for the poor a bad name. High rises can work well, so long as they are well maintained and managed (some of the most desirable places to live in Chicago, Vancouver, Hong Kong and, of course, New York are high rises). More important, the complex lent such a stigma to public housing that it eliminated it as a mechanism to house the poor.

Malpezzi and I have written that the public housing that the US has built has been invariably inefficient as a means for housing low-income people in expensive American cities. This doesn't necessarily mean that it must be so, but the disasters of Pruitt-Igoe and other large scale public housing projects (Cabrini-Green and Robert Taylor Homes in Chicago are almost as notorious) means we might never find differently.

Wednesday, December 20, 2006

Wednesday, December 13, 2006

Recruiting for MBAs in the Middle East

I am home from recruiting MBA students in Dubai and Cairo.

Cairo is one of the greatest cities I have ever visited; the architecture, street life, and, oh yes, the antiquities are beyond compare. The people there were exceptionally hospitable, and the streets are safe, if heavily littered. I bought some cool if corny papyrus paintings; the Nefertiti will hang in honor next to my velvet Elvis.

I met great potential students in both Dubai and Cairo, and would love to bring at least a half-dozen from each place to George Washington. The sticking point, in their minds, was getting a student visa. The perception was that getting student visas to the US is too much of a hassle; as a friend of mine at National University of Singapore said to me, the difficulty in getting visas to the US has made recruiting at NUS much easier. Don't get me wrong, NUS is terrific (I have very much enjoyed my two visits there), but I would rather students come here.

My reasons for this are not entirely altruistic. I think having college and graduate students coming to the United States is extremely important to our image in the World. While people in Egypt complained bitterly about US Middle-East foreign policy, they nevertheless wanted to come to America. In the 17 years I have been teaching (has it been that long?), I have seen generation upon generation of international students transformed by their experience in America--and transformed for the better. Once students are here for a few years, they often appreciate America's openness, and generosity, and they embrace American ideals. They can't help but feel better about America's place in the world, even as they continue to oppose US foreign policy. In some small way, this must leave us safer.

A State Department Official in Cairo told me he get could get visas for students accepted at US universities in 3 days. If this is really true, I am optimistic about increasing the flow of students from Morocco to Jordan to Oman into the United States. This would benefit us all.

On my eight day trip, I took one morning off. This is what I saw:

I would say that if you get a chance to see one wonder in your life, this should be it. Astonishing.

I would say that if you get a chance to see one wonder in your life, this should be it. Astonishing.

Tuesday, December 05, 2006

Mumbai

I am currently in Mumbai, recruiting MBA students. This is my second trip to this marvelous, vibrant, horrible city. When I walk the streets here, I think about Dickens' London.

The city is remarkably entrepreneurial . There are people selling stuff everywhere, and lots of cottage industry, even in the slums. Kids are going to school here in much larger numbers than 30 years ago, and so literacy has risen dramatically. One sees fashionable shops, and the street along the sea, Marine Drive, could become among the most attractive in the world, comparable to Lake Shore Drive in Chicago.

Yet it is a city of eight million in which 20 percent have no access to toilets; in which the largest slum in the world sits; in which commuter trains run with 4 to 5 times the number of passengers for which they were designed; in which live many pavement dwellers. Many workers do unspeakably difficult tasks--such as breaking up old ships with hammers--for about $2 per day.

Some of the horrors here are a function of the fact that this remains a city that, despite substantial progress, remains extraordinarily poor. But land use policy here makes things worse. Two issues stand out in particular. First, government and quasi government enterprises own vast swatches of land here--the old port is one example. To say this land is underutilized is a severe understatement. Mumbai badly needs to use its developable land--right now land here is as expensive as it is in Montgomery County Maryland, while incomes here are about 1/50th of what they are in Montgomery County.

Second, there is a hostility here to tall buildings. But the Mumbai peninsula, with 150,000 people per square mile, is twice as dense as Manhattan. The only way people can be housed reasonably here is to build up. High rise housing had a bad reputation, I think, because of the ugliness perpetrated in the former Soviet and Soviet-satellite cities. East Berlin was not very attractive (nor was most of the high-rise public housing built in the US). But Hong Kong, Singapore, New York and Chicago demonstrate that high rise housing can be attractive. Shanghai has used high-rise housing to rapidly improve housing conditions there in the past 15 years.

One could talk about a lot of other things Mumbai needs to do to move forward--infrastructure development--including good sidewalks--needs to be on the top of the list. But giving people more room to live might do more than anything else to improve living conditions here.

New President at George Washington!

We have a new president: Steven Knapp, who is currently provost at Johns Hopkins. I was hoping against hope that our new leader would be the provost of a World-class research university, and that is exactly what we got. I am excited.

Sunday, December 03, 2006

Monday, November 27, 2006

To keep blogger status

I gave a seminar on urban economics today at the George Washington Institute for Public Policy. I learned that to be a true blogger, I must post at least once a month, so here I am.

I am trying to figure out how soft the housing market has gotten. One of the problems--the two best known data sets for looking at house prices--the NAR median house price set and the OFHEO repeat sales index--are moving in opposite directions. The NAR data probably reflect the way the assign regional weights for determining house prices, but there are still cities where the NAR data show price declines, while OFHEO shows increases.

More tomorrow.

I am trying to figure out how soft the housing market has gotten. One of the problems--the two best known data sets for looking at house prices--the NAR median house price set and the OFHEO repeat sales index--are moving in opposite directions. The NAR data probably reflect the way the assign regional weights for determining house prices, but there are still cities where the NAR data show price declines, while OFHEO shows increases.

More tomorrow.

Monday, October 30, 2006

Airports and Economic Development

Before the 18th Century, harbors mattered a lot. They allowed trade, and explain why the cities in the current Netherlands became rich, despite the relative lack of natural recourses. In the 19th Century, canals and railroads were important. More recently, highways have mattered a lot--Ed Glaeser has written on how highway spending helps explain differences in urban growth.

But airports may be what harbors once were. I have a recent paper that looks at differences in population and employment growth across metropolitan areas: education matters, climate matters, and airports matter, a lot.

Here is the paper's conclusion:

The paper is available on the GW Web Site. http://www.gwu.edu/~business/research/workingpapers/Airport%20GW.pdf

But airports may be what harbors once were. I have a recent paper that looks at differences in population and employment growth across metropolitan areas: education matters, climate matters, and airports matter, a lot.

Here is the paper's conclusion:

This paper sought to find a relationship between airport activity and economic development, and it found one. Passenger boardings per capita and passenger originations per capita in the nation’s largest metropolitan areas are powerful predictors of population growth and employment growth. This is the case after a number of controls are put in place, and survives after an attempt to control for simultaneity issues. Beyond statistical significance, the magnitude of the coefficient on boardings per capita indicates that the magnitude of the effect of passenger boardings on these two measures of economic development could be rather large. It might particularly suggest that where airports are constrained by capacity (such as they are in Chicago, Boston, New York and Los Angeles), adding to capacity might well have an important economic development impact. That said, these results do not suggest that every small city should run out and build a large airport.

Of course the results presented here are far from conclusive: they are, perhaps, among the first of their kind (this paper was written contemporaneously with Brueckner 2003), and are therefore subject to far more scrutiny. Nevertheless, their statistical significance is sufficiently strong that it survives a large variety of alternative specifications. The results are also consistent with the findings in Brueckner.

The policy implications of this finding are therefore quite important. The political economy of airports is very much a function of their governance structure. The cost (at least the perceived cost) of airports to members of a community is highly concentrated geographically, while the benefits tend to be diffused throughout the community. Airports are sometimes under the control of local units of government, such as city councils or county boards. When this is the case, representatives whose districts include an airport have a strong incentive to become members of the airport authority. Consequently, decisions about airports can be based on parochial interests, even if the total benefits of the airport to the economy exceed the cost. Should air traffic be a large determinant of economic success, it is entirely possible that the benefits of new or expanded airports exceed costs.

Yet we have observed that in many places (San Francisco, Boston, Milwaukee), interest groups have worked to inhibit runway expansion, while in other places (Chicago), local political squabbles have prevented any number of potentially reasonable plans for expanding airport capacity from going forward in a timely manner. All this suggests that airport policy might best be made regionally, rather than locally. Of course, the regional policy would have to include a scheme for compensating those injured by airport expansion. But if the regional benefits of airport development are large, the costs of fair compensation should be easy to finance.

The paper is available on the GW Web Site. http://www.gwu.edu/~business/research/workingpapers/Airport%20GW.pdf

Monday, October 23, 2006

Bridges

Slate today has gorgeous pictures of my favorite bridge--the George Washington Bridge. The bridge is a masterpiece of architecture and engineering, and was completed at the time my father was born. It also helped create suburban New Jersey.

Bridges seem politically unpopular right now--they only seem to get built (or proposed) where they aren't necessary. In my town, for instance,

there has not been an additional bridge built across the Potomac in nearly 40 years, despite the fact that the metropolitan area has doubled in size. The lack of bridges has created choke-points in the regional transportation system; choke-points that make people unhappy throughout the region, but that people don't seem to want to do anything about. I would guess that a couple of more bridges from the District into Arlington would easily pass any cost-benefit test, but they flunk the political test.

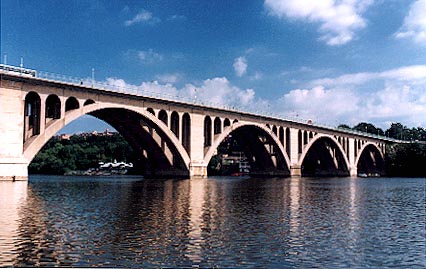

there has not been an additional bridge built across the Potomac in nearly 40 years, despite the fact that the metropolitan area has doubled in size. The lack of bridges has created choke-points in the regional transportation system; choke-points that make people unhappy throughout the region, but that people don't seem to want to do anything about. I would guess that a couple of more bridges from the District into Arlington would easily pass any cost-benefit test, but they flunk the political test.Perhaps the reason for this is that we built too many ugly bridges. The older bridges across the Potomac--Memorial Bridge, Key Bridge and Chain Bridge--are all quite beautiful. Don't take more word for it--the picture on top is of Key Bridge, the one just below it is Memorial Bridge.

Compare these with the 14th Street Bridge:

It is not hard to understand why people don't want more of these.

But bridges have made lives better for people--they have relieved congestion and, because they open up more urban land for development--reduced housing costs. While some urban planners sniffed that the post World War II suburbs of New Jersey and Long Island and Northern Virgina were banal, they also allowed the emerging middle class the ability to own houses at reasonable cost. These places would not exist in the absence of bridges.

Monday, October 09, 2006

In the Department of Self-Promotion

I am quoted in Robert J. Samuelson's newsweek column.

http://www.msnbc.msn.com/id/15173465/site/newsweek/page/2/

http://www.msnbc.msn.com/id/15173465/site/newsweek/page/2/

Thursday, October 05, 2006

Wednesday, October 04, 2006

Case-Shiller, Ofheo, etc.

This is a really wonky post, but after talking with a reporter today about house price indices, I couldn't help myself. The most commonly cited "constant quality" house price indices come from Case and Shiller, and from the Office of Federal Housing Enterprise oversight. These indices attempt to follow the price of a particular house at a particular place over time. To explain how they work, I will lift from my book with Steve Malpezzi:

Case-Shiller actually does a better job of keeping quality constant than OFHEO, but OFHEO has more coverage (I think). I will explain why in another post.

Repeat Sales Price Indexes

Repeat sales indexes are estimated by analyzing data where all units have sold at least twice. Such data allow us to annualize the percentage growth in sales prices over time. These are time-series indexes in their pure form. They do not provide information on the value of individual house characteristics or on price levels. They have the advantage of being based on actual transaction prices, and in principle allow us to sidestep the problem of omitted variable bias. However, units that sell are not necessarily representative of all units. Sometimes it's difficult to tell whether a unit retains the same characteristics across time. For example, remodeling could change a house’s characteristics.

The best way to understand how repeat sales indexes work is to look at an example. Figure 2.15 shows a graph of 17 properties that sold twice in the Shorewood Hills neighborhood of Madison, Wisconsin, in the late 1980s and early 1990s. Each property is numbered from 1 to 17, and each property appears twice. The Y-axis is the logarithm of the selling price of the unit.

We can think of the repeat sales estimator as an attempt to measure the average slope of the lines in Figure 2.15, year by year. In a classic paper, Bailey, Muth, and Nourse (1963) illustrated how to compute this using regression methods and a larger sample.

One way to motivate the actual technique used to construct the repeat sales index is to start by reconsidering the hedonic model. Consider a simple semilog hedonic equation

ln P = Xb + b1D1 + b2D2 + b3D3 + b4D4

where P is the value or rent for the unit, and where the vector X includes all the relevant characters, including a constant term; and the time dummies Di represent periods that follow the initial base case period.

The vector X represents a list of housing and neighborhood characteristics that would enter a hedonic equation. The vector D is a series of dummy variables representing the time periods under consideration. These could be months, quarters, or years, depending upon the type of data at hand.

Consider a house, “A,” that sells in periods 2 and 4 (period 0 is the base year). In period 2, we calculate:

ln PA2 = Xb + b1D1 + b2D2 + b3D3 + b4D4

= Xb + b2D2

since D1, D3, and D4 = 0. And of course, by similar reasoning, in period 4:

ln PA4 = Xb+ b4D4

Then, by subtraction, we find:

ln PA4 - ln PA2 = Xb + b4D4 - Xb - b2D2

= b4D4 - b2D2

This is for a representative housing unit that sells twice. Given a sample of such units, we want, in effect, the “average” b4 and b2. (Recall that regression is, in effect, estimating a series of conditional means.) Clearly, by subtraction, the characteristics vector drops out, as do the dummy variables for periods in which no transaction takes place.

Case-Shiller actually does a better job of keeping quality constant than OFHEO, but OFHEO has more coverage (I think). I will explain why in another post.

Tuesday, September 26, 2006

Long-term interest rates again

This morning's Wall Street Journal reports that long-term interest rates are at their lowest levels in months, with the ten-year Treasury at 4.55 percent. They also note:

The MBA has been ahead of the curve in figuring out how the inverted yield curve would affect refinancing. This should help soften price declines in the housing market, particularly in markets away from the coasts.

Nevertheless, yesterday's news on prices and inventories out of NAR was ugly: prices are falling a bit, and inventories are at a high for the decade.

Recent data from the Mortgage Bankers Association suggests that some families have taken advantage of a decline in long-term mortgage rates to refinance their mortgages and lock in lower payments. The association's index of mortgage refinancing applications has risen 27% since mid-July, and now stands at its highest level since February.

The MBA has been ahead of the curve in figuring out how the inverted yield curve would affect refinancing. This should help soften price declines in the housing market, particularly in markets away from the coasts.

Nevertheless, yesterday's news on prices and inventories out of NAR was ugly: prices are falling a bit, and inventories are at a high for the decade.

Sunday, September 24, 2006

A Key to a Soft Landing in Housing

As I have already mentioned, the Chicago Merc housing futures market is predicting a decline in nominal house prices in several markets over the next year. While the market is still very thinly traded, it likely reflects a prevailing view among many investors and observers of the housing market.

One of the reasons for the softening of in some markets has been the increase in the federal funds rate. Some work in progress among Chris Redfearn, Stuart Gabriel and me is showing that the short end of the yield curve migh have a substantial impact on house prices in many of the coastal cities. The reason: in expensive markets, borrowers slide down to the short end of the yield curve where the cost of borrowing is generally lower. This allows borrowers to buy houses with "affordable" initial payment-to-income ratios.

The problem, of course, is that short term interest rates have been driven up by the Federal Reserve, from one percent in late 2003 to 5.25 percent today. If an Adjustable Rate Mortgage's spread over the fed funds rate is three percent (not usually the way ARMs are calculated, but lets give the example to make a point), and it amorizes over 30 years, the payment on an ARM would rise more than 50 percent per dollar of mortgage balance. This means people who could get into the housing market in a place like Los Angeles before can no longer do so, and it means many people in Los Angeles are facing payment shock. The situation is even worse for those who used "option ARMs" to finance their houses--these products allow people to pay less than the interest they owe on their mortgage every month, meaning that their loan balances are rising over time.

The good news is that long-term fixed rate mortgages, while not at rock bottom rates, remain at very low rates by the standard of the past 25 years: 30 year-fixed rate conforming mortgages last week hast week at an average rate 6.4 percent, according to Freddie Mac's survey. This means the ARM borrowers can refinance out of their ARM into a fixed rate product that is pretty reasonable. This should place a floor under house prices, particularly in an economy where unemployment is pretty low.

I think the early part of the '00s should have taught an important lesson to homebuyers--if they can't afford a house with a 30 year fixed-rate mortgage, they probably shouldn't buy a house. That is not to say the ARM isn't a good product--it is, if households use it as part of a portfolio strategy. For instance, is someone knows she is only going to live in a city for five years, it is perfectly reasonable for her to borrower with a 5/1 ARM, where the rate is fixed for only five years. Her liability, the mortgage, now matches her asset, the house, where she expects to live for five years. But when people use ARMs--especially option ARMS--to make payment-to-income ratios acceptable for a limited period of time, they are liekly looking for trouble.

One of the reasons for the softening of in some markets has been the increase in the federal funds rate. Some work in progress among Chris Redfearn, Stuart Gabriel and me is showing that the short end of the yield curve migh have a substantial impact on house prices in many of the coastal cities. The reason: in expensive markets, borrowers slide down to the short end of the yield curve where the cost of borrowing is generally lower. This allows borrowers to buy houses with "affordable" initial payment-to-income ratios.

The problem, of course, is that short term interest rates have been driven up by the Federal Reserve, from one percent in late 2003 to 5.25 percent today. If an Adjustable Rate Mortgage's spread over the fed funds rate is three percent (not usually the way ARMs are calculated, but lets give the example to make a point), and it amorizes over 30 years, the payment on an ARM would rise more than 50 percent per dollar of mortgage balance. This means people who could get into the housing market in a place like Los Angeles before can no longer do so, and it means many people in Los Angeles are facing payment shock. The situation is even worse for those who used "option ARMs" to finance their houses--these products allow people to pay less than the interest they owe on their mortgage every month, meaning that their loan balances are rising over time.

The good news is that long-term fixed rate mortgages, while not at rock bottom rates, remain at very low rates by the standard of the past 25 years: 30 year-fixed rate conforming mortgages last week hast week at an average rate 6.4 percent, according to Freddie Mac's survey. This means the ARM borrowers can refinance out of their ARM into a fixed rate product that is pretty reasonable. This should place a floor under house prices, particularly in an economy where unemployment is pretty low.

I think the early part of the '00s should have taught an important lesson to homebuyers--if they can't afford a house with a 30 year fixed-rate mortgage, they probably shouldn't buy a house. That is not to say the ARM isn't a good product--it is, if households use it as part of a portfolio strategy. For instance, is someone knows she is only going to live in a city for five years, it is perfectly reasonable for her to borrower with a 5/1 ARM, where the rate is fixed for only five years. Her liability, the mortgage, now matches her asset, the house, where she expects to live for five years. But when people use ARMs--especially option ARMS--to make payment-to-income ratios acceptable for a limited period of time, they are liekly looking for trouble.

Tuesday, September 19, 2006

America the Spacious

While those of us who live on the Eastern seaboard of the United States feel hemmed in, the fact is that by World urban standards, we have a lot of space.

One of my favorite websites is http://alain-bertaud.com/. Alain has a wonderful gathering of information on urban environments around the world. Among his many great graphs, a particularly revealing one is the one to the left: it gives average urban densities for large cities around the world.

Note that American cities are in red: the densest of this, of course, is New York. But New York is less dense than European cities, and is much less dense than Asian and African cities. My home city of Washington is practically rural compared with most large cities around the world. But then, I am sure that someone from Mumbai would consider suburban Maryland and Virginia to be the countryside.

One of the reasons American cities have so little density is that the United States has a lot of land (only about five percent of which is developed) ; another reason is that the US is a rich country, and rich people buy more stuff, including land. But these reasons are only part of the story. More to come....

Sunday, September 17, 2006

Jon Stewart on Social Foment

We saw Jon Stewart at Merriweather Post Pavillion last night. He articuated well why many of us can't get organized about expressing our frustration at policy and policy makers. The rallying cry of "be reasonable" somehow does not have an inspirational ring to it.

Credit to Francois Ortalo-Magne

It occurs to me that I might never have come up with the idea in the previous post had it not been for a conversation I had with Francois Ortalo-Magne at an NBER conference around a month ago. Francois pointed out the selectivity problem in Levitt's work.

Friday, September 15, 2006

Do Real Estate Brokers Shirk?

Steve Levitt is an incredibly smart guy (he has a Clark Medal, the prize for best economist under 40, to prove it) and, according to the people I know who know him, a very nice guy. Freakonomics is fun to read, and I liked it enough to use it for a seminar I taught last summer.

A reason the book is so much fun is that it is provocative, and challenges us to think about things from perspectives we had not before considered. It asks why drug dealers live with their mothers; whether Roe v Wade was responsible for the falling crime rate in the 1990s; whether Sumo Wrestlers cheat; and whether real estate agents shirk.

Levitt sets up the real estate agent-house seller relationship as a classical principal-agent problem: the agent is like anyone else: he has an incentive to do as little work as possible in exchange for as much commission as possible. Therefore, Levitt conjectures that real estate agents have an incentive to get sellers to take the first offer they receive from buyers. Because commissions are based on the entire price of the house, the fact of a sale gives agents a large benefit. If the seller refuses an offer, the agent has to do more work, but gets very little added compensation. For example, if there is a $490,000 offer on a house that could ultimately sell for $500,000, and the agent gets a 1.5 percent cut, from the standpoint of the agent, the benefit of waiting is only $150. The agent will almost certainly have to do a lot more work for the $150, and so has an incentive to encourage the buyer to take the $490k.

This would be a powerful argument for an incentive problem if agents were playing a one-shot game. But they are not--they are playing a repeated game. Agents rely on listings to make money, and listings come from referrals. Agents--good ones anyway--have an incentive to make sellers very happy, because happy sellers drive future business.

So now let's get to the evidence that Levitt provides to show that agents shirk: he shows that agents leave their own houses on the market longer and sell them for higher prices than the houses that they sell for others. This is an interesting fact, but is not necessarily explained by agents' shirking. Rather, it could be that the houses agents own themselves are different in unobserved characteristics from the houses that they sell to others. Or it could be that agents are different as human beings--they are more risk taking, and more entrepreneurial. For all we know, sellers ignore the advice of their agents and sell more quickly than they should, because they are relieved at the prospect of a sale and don't care so much about the marginal benefit they would get for waiting. In order to disentangle this, we would need to know something about the unobserved characteristics of people who become real estate agents--and of people who don't.

Full disclosure: while I was writing my dissertation in the late 1980s, I worked doing research for the Wisconsin Realtors Association. I had fun while I was there. Believe me, the Realtors are different with respect to their attitude toward risk taking from the rest of us.

A reason the book is so much fun is that it is provocative, and challenges us to think about things from perspectives we had not before considered. It asks why drug dealers live with their mothers; whether Roe v Wade was responsible for the falling crime rate in the 1990s; whether Sumo Wrestlers cheat; and whether real estate agents shirk.

Levitt sets up the real estate agent-house seller relationship as a classical principal-agent problem: the agent is like anyone else: he has an incentive to do as little work as possible in exchange for as much commission as possible. Therefore, Levitt conjectures that real estate agents have an incentive to get sellers to take the first offer they receive from buyers. Because commissions are based on the entire price of the house, the fact of a sale gives agents a large benefit. If the seller refuses an offer, the agent has to do more work, but gets very little added compensation. For example, if there is a $490,000 offer on a house that could ultimately sell for $500,000, and the agent gets a 1.5 percent cut, from the standpoint of the agent, the benefit of waiting is only $150. The agent will almost certainly have to do a lot more work for the $150, and so has an incentive to encourage the buyer to take the $490k.

This would be a powerful argument for an incentive problem if agents were playing a one-shot game. But they are not--they are playing a repeated game. Agents rely on listings to make money, and listings come from referrals. Agents--good ones anyway--have an incentive to make sellers very happy, because happy sellers drive future business.

So now let's get to the evidence that Levitt provides to show that agents shirk: he shows that agents leave their own houses on the market longer and sell them for higher prices than the houses that they sell for others. This is an interesting fact, but is not necessarily explained by agents' shirking. Rather, it could be that the houses agents own themselves are different in unobserved characteristics from the houses that they sell to others. Or it could be that agents are different as human beings--they are more risk taking, and more entrepreneurial. For all we know, sellers ignore the advice of their agents and sell more quickly than they should, because they are relieved at the prospect of a sale and don't care so much about the marginal benefit they would get for waiting. In order to disentangle this, we would need to know something about the unobserved characteristics of people who become real estate agents--and of people who don't.

Full disclosure: while I was writing my dissertation in the late 1980s, I worked doing research for the Wisconsin Realtors Association. I had fun while I was there. Believe me, the Realtors are different with respect to their attitude toward risk taking from the rest of us.

Wednesday, September 13, 2006

Ofheo House Price Index Flattens

See http://www.ofheo.gov/media/pdf/2q06hpi.pdf. House prices rose only 1.17 percent in the second quarter, according to the index. This is an increase that more or less keeps pace with inflation.

The Ofheo house price index is not, however, completely representative of the housing market. Ofheo tracks prices on houses financed by Fannie Mae and Freddie Mac; Fannie and Freddie may only finance "conforming" loans, which are in 2006 defined as loans whose value is less than 417,000. This limit shuts Fannie and Freddie off from large parts of the California, Boston, New York and Washington housing markets; consequently, should these large markets go into the tank, their impact on the index will be muted.

The Case, Shiller, Weiss (http://www2.standardandpoors.com/servlet/Satellite?pagename=sp/Page/PressSpecialCoveragePg&c=sp_speccoverage&cid=1143857726920&r=1&l=EN&b=4index ) doesn't have this issue; nor, presumably, do the indexes that one can find in Zillow. The CSW Composite Index for 10 cities was completely flat in June.

The Ofheo house price index is not, however, completely representative of the housing market. Ofheo tracks prices on houses financed by Fannie Mae and Freddie Mac; Fannie and Freddie may only finance "conforming" loans, which are in 2006 defined as loans whose value is less than 417,000. This limit shuts Fannie and Freddie off from large parts of the California, Boston, New York and Washington housing markets; consequently, should these large markets go into the tank, their impact on the index will be muted.

The Case, Shiller, Weiss (http://www2.standardandpoors.com/servlet/Satellite?pagename=sp/Page/PressSpecialCoveragePg&c=sp_speccoverage&cid=1143857726920&r=1&l=EN&b=4index ) doesn't have this issue; nor, presumably, do the indexes that one can find in Zillow. The CSW Composite Index for 10 cities was completely flat in June.

Monday, September 11, 2006

A Paper on Market Reaction to 9/11 by Kallberg, Liu and Pasquariello

I really like this paper:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=716721

Abstract:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=716721

Abstract:

This study analyzes how three groups of market participants - insiders, analysts, and investors - revised their expected returns on New York Real Estate Investment Trusts (REITs) in response to the catastrophic events of September 11, 2001. The attack on the WTC represents a unique experimental setting to evaluate financial markets' reaction to external shocks for several reasons. First, these events, of a totally unanticipated and unprecedented nature, could not have been built into the market's expectations; hence, market participants had to learn something new rather than just recalibrate their expectations on past occurrences. Second, unlike other studies of market reactions, the impact of the terrorist attacks on REIT returns was ambiguous, since it was uncertain if the effect of reduced supply of office space in New York would outweigh the impact of the negative shocks to the local and national economy on its demand. Finally, the period of market closure that followed 9/11 gave these players ample opportunity to reassess their expectations. Our analysis reveals that, on the day when markets reopened, REITs with significant exposure to the New York area outperformed a broad REIT office index by 4.1%. However, we find that, according to several metrics of real market behavior, this anticipated superior performance of New York office properties did not materialize. Consistent with notions of market efficiency, we find that insiders were the first to lower their expectations (99.9% of their trades in REITs with New York exposure were sales in the month following 9/11), followed by analysts (the vast majority of them revised downward their expectations of NY REIT performance in the first weeks of November 2001), and finally market prices adjusted to reflect the underlying real market behavior; indeed, abnormal REIT returns had disappeared by mid November 2001.While the paper is principally about information diffusion, it also presents some very nice data on the resiliency of the New York employment market in the wake of 9/11. New York's refusal to be cowed may be the greatest victory we have had over Al-Qaeda. But that refusal also speaks volumes about why New York became a great city in the first place.

Monday, September 04, 2006

The Chicago Merc Housing Futures Market

Chip Case and Robert Shiller have created a housing futures market for 10 US cities, along with a composite of those cities, that trades on the Chicago Mercantile exchange. If it works, it will allow homeowners to diversify some of their risk, and presumably make the market more liquid.

Owners who have lots of of home equity are long in the housing market. This may be fine, but it also may be that their length in housing means that they are not as diversified into other assets as they may wish. The CME index can help.

Here is how it works. Suppose you own a house in Washington, D.C. The most recent index value for Washington is from June, and is 250.39. The next futures contract is for November, and currently has a price of 247.8. If you take a short position for November, you have the right to sell the Washington index at 247.8 per unit. If the value of your house us perfectly correlated with the index, you can completey immunize yourself from swings in the market, outside of the difference between the June index and November price. If the price falls below 247.8, the profit on your short position will offset the loss in house value; if the price rises above the 247.8, your house offsets the loss on your short position. All of this assumes that there are no tax implications, but even with taxes, the index enables homeowners to at least partially hedge their risk.

All of this should actually make houses more valuable, because it should increase liquidity in the housing market. There remain some issues--chief among them is the lack of a true spot market in housing, because of the lag in the time between when a house receives an offer and when it actually settles. I'll discuss this further in another post. I will also discuss what the futures markets are saying about the future of house prices, and the implications for the own-rent decision.

Owners who have lots of of home equity are long in the housing market. This may be fine, but it also may be that their length in housing means that they are not as diversified into other assets as they may wish. The CME index can help.

Here is how it works. Suppose you own a house in Washington, D.C. The most recent index value for Washington is from June, and is 250.39. The next futures contract is for November, and currently has a price of 247.8. If you take a short position for November, you have the right to sell the Washington index at 247.8 per unit. If the value of your house us perfectly correlated with the index, you can completey immunize yourself from swings in the market, outside of the difference between the June index and November price. If the price falls below 247.8, the profit on your short position will offset the loss in house value; if the price rises above the 247.8, your house offsets the loss on your short position. All of this assumes that there are no tax implications, but even with taxes, the index enables homeowners to at least partially hedge their risk.

All of this should actually make houses more valuable, because it should increase liquidity in the housing market. There remain some issues--chief among them is the lack of a true spot market in housing, because of the lag in the time between when a house receives an offer and when it actually settles. I'll discuss this further in another post. I will also discuss what the futures markets are saying about the future of house prices, and the implications for the own-rent decision.

Sunday, September 03, 2006

A discussion on the Income Distirbution

From Brad Delong's Blog:

http://delong.typepad.com/sdj/2006/09/making_em_feel_.html

The first comment from readers seems on target to me. If we wish to encourage innovation, but discourage "spiteful" consumption, then using a luxury tax, instead of a more progressive income tax, makes sense. But does this mean that people would have to pay a tax for going to Greg Mankiw's high tuition university, but not pay that tax for going to Brad Delong's low-tuition university?

http://delong.typepad.com/sdj/2006/09/making_em_feel_.html

The first comment from readers seems on target to me. If we wish to encourage innovation, but discourage "spiteful" consumption, then using a luxury tax, instead of a more progressive income tax, makes sense. But does this mean that people would have to pay a tax for going to Greg Mankiw's high tuition university, but not pay that tax for going to Brad Delong's low-tuition university?

Some Reading for Friday's Commercial Real Estate "bootcamp" at GW.

Here are a first set of readings. More readings and commentary will be coming shortly.

http://www.irei.com/uploads/marketresearch/65/marketResearchFile/SORetail_Mkt_Inv_Opp7-06.pdf

http://www.irei.com/uploads/marketresearch/35/marketResearchFile/Pru_USQuarterly_July%2006.pdf

http://www.irei.com/uploads/marketresearch/10/marketResearchFile/RealEstateCapRates.pdf

http://www.irei.com/uploads/marketresearch/65/marketResearchFile/SORetail_Mkt_Inv_Opp7-06.pdf

http://www.irei.com/uploads/marketresearch/35/marketResearchFile/Pru_USQuarterly_July%2006.pdf

http://www.irei.com/uploads/marketresearch/10/marketResearchFile/RealEstateCapRates.pdf

Thursday, August 31, 2006

What is a "Land of Opportunity?"

I just heard Clive Crook on NPR describing new research that shows that by one measure, the United States falls behind Finland, Sweden and France (yes, France) as a land of opportunity. The measure? How well a parent's income predicts his or her offspring's income. Presumably, if we all started out even, if our parents didn't matter, there would be no correlation in income across generations.

But why do kids of the affluent do well in the US? Is it a Paris Hilton effect? Perhaps. If this were the whole story, then America's claim as a land of opportunity is on shaky groud. My suspicion is that things are more complicated.

I happen to live in one of the most affluent counties in the United States--Montgomery County, Maryland. The reason I live here, instead of the District of Columbia, is that the schools here are excellent. One of the reasons that the schools are excellent is that the kids in these schools are amazing. I never fail to be impressed by the work ethic of my sixteen-year olds' circle of classmates. These kids, whose parents are by and large pretty well off, will be by and large well off themselves. Their affluence will not come from clipping bond coupons with golden scissors, but rather from the fact that they will be valuable in the labor force. And as the world globalizes, people with rare skills will become more valuable, as their abilities affect more people.

Paul Krugman suggests that it is policy, rather than productivity, that has led the income distribution to become more skewed, and has reduced social mobility. One wag supported this notion by pointing out that Paul Krugman makes far more money than James Tobin ever did, even though Tobin was a greater economist.

Tobin was the better economist, but Krugman is more productive, because his ideas reach a much broader group of people--technology had enhanced Krugman's productivity and therefore his salary. People with high levels of education and unusual gifts are more valuable than they have ever been. Well educated parents have a particular incentive to make sure that their children gain both the attitudes and credentials necessary for success.

But in the end, this is unfair to those whose parents are at the bottom of the income ladder. Among other things, they cannot afford to live in those parts of metropolitan areas where the schools are excellent. Let me share something I wrote for the Congress on New Urbanism:

But why do kids of the affluent do well in the US? Is it a Paris Hilton effect? Perhaps. If this were the whole story, then America's claim as a land of opportunity is on shaky groud. My suspicion is that things are more complicated.

I happen to live in one of the most affluent counties in the United States--Montgomery County, Maryland. The reason I live here, instead of the District of Columbia, is that the schools here are excellent. One of the reasons that the schools are excellent is that the kids in these schools are amazing. I never fail to be impressed by the work ethic of my sixteen-year olds' circle of classmates. These kids, whose parents are by and large pretty well off, will be by and large well off themselves. Their affluence will not come from clipping bond coupons with golden scissors, but rather from the fact that they will be valuable in the labor force. And as the world globalizes, people with rare skills will become more valuable, as their abilities affect more people.

Paul Krugman suggests that it is policy, rather than productivity, that has led the income distribution to become more skewed, and has reduced social mobility. One wag supported this notion by pointing out that Paul Krugman makes far more money than James Tobin ever did, even though Tobin was a greater economist.

Tobin was the better economist, but Krugman is more productive, because his ideas reach a much broader group of people--technology had enhanced Krugman's productivity and therefore his salary. People with high levels of education and unusual gifts are more valuable than they have ever been. Well educated parents have a particular incentive to make sure that their children gain both the attitudes and credentials necessary for success.

But in the end, this is unfair to those whose parents are at the bottom of the income ladder. Among other things, they cannot afford to live in those parts of metropolitan areas where the schools are excellent. Let me share something I wrote for the Congress on New Urbanism:

Urban Location and Schools

Richard K. Green

The George Washington University

Neighborhoods within cities are heterogeneous; municipalities within metropolitan area are heterogeneous too. The racial and income composition of individual neighborhoods in diverse cities is rarely similar to the composition of the cities in which they lie. For example, the average poverty rate in Washington, D.C. and its proximate counties (Arlington, Fairfax and Alexandria City, Virginia and Montgomery and Prince George’s County, Maryland) was 8.2 percent in 2000; but the rate ranged from 4.5 percent in Fairfax County to 20 percent in the District. Within the District itself, census tract level poverty rates ranged from around one percent to over 70.

The reasons for this variation are myriad. Perhaps the most important reasons for this variation have nothing directly to do with schools: the availability of affordable housing and the cost of transportation. William Alonso, in a classic paper, uses a simple theoretical model that predicts that in a world of high fixed transportation costs, the poor will settle in a city’s center. The reason: by living close to jobs, neighbors and services, the poor avoid transportation costs. In exchange, they consume little in the way of housing, and live very densely. While this leads to housing being relatively inexpensive, the cost they spend per unit of housing services they receive is high. That is, while total rent in the middle of Philadelphia is relatively inexpensive, the houses people are renting may be in disrepair—all of the rent is going to pay for location.

But it is also true that low income people may be constrained to live in urban centers because of a phenomenon William Fischel termed fiscal zoning. Local officials have an incentive to please the median voter in their communities by maximizing services relative to taxes. One tool for doing this is zoning that assures that the least expensive houses are very expensive indeed. Some communities ban apartments; others have large minimum lot size requirements. This combination creates a large per capita tax base and leads to high quality services being capitalized into property values. But it also locks low income people out.

A crude, but easy method, for demonstrating how settlement patterns have played out is to look at the household shares of single women with children and married couples with children in some cities and immediately adjacent suburbs.

Central City County Unmarried Female with Children Share Married Couple with Children Share Suburban County Unmarried Female with Children Share Married Couple with Children Share

Orleans 14.0 16.5 Jefferson 7.2 27.7

Suffolk 9.1 13.6 Middlesex 4.4 24.5

San Francisco 4.3 13.8 San Mateo 4.1 24.5

Philadelphia 9.8 16.9 Montgomery 3.1 28.0

St. Louis 12.0 12.8 St. Louis County 5.3 26.8

Denver 6.7 15.6 Jefferson 5.4 30.1

The poverty rate among married couples with children is low—around 6 percent, or about half the national rate. But the poverty rate among unmarried with children is nearly 35 percent. So the combination of urban land prices, transportation costs and fiscal zoning has led to income heterogeneity in settlement patterns.

While schools may not in themselves be the primary cause of these settlement patterns, the implications of these patterns for schools are important. The ability of low income people to choose to live in areas with good schools is limited by economic considerations apart from school, or by zoning. Conversely, families of means have the ability to choose economically feasible neighborhoods and schools jointly. Let us be clear—school choice is already available to people with money. This lesson came home to me when my family moved to metropolitan Washington; my wife and I were in the fortunate position of being able to choose the public schools our children would attend. The choice set broadened further when my children decided to attend a magnet high school outside of their local school district.

It is unfair that geography allows only some families to choose where their children go to school. Among other things, it means that almost all students at some schools come from families whose choices are limited. A large number of studies (including one by conference participant Thomas Nechyba and his Duke colleague Jacob Vignor) have demonstrated the importance of peer effects—who one goes to school with matters. Of particular interests are findings that students who go to school with peers who have a variety of abilities may perform better, controlling for average level of ability, than those who go to homogeneous schools. Economic and zoning conditions force some families to send their children to schools with students whose performance is both homogeneous and low.

An appropriate policy response to this is to decouple school choice from geography. School vouchers are one method for doing this; charter schools are another; magnet schools are a third—all are worth trying. The Experimental Housing Allowance Program demonstrated that housing vouchers were an efficient and effective method for providing low-income people with housing. The current experiments with choice and charter schools could well prove to me even more important.

Wednesday, August 30, 2006

Assessment of Education

My colleague Mary Gowan is passionate about the importance of assessment in eduction. Derek Bok, in Our Underachieving Colleges, articulates why it is important:

But this is not enough. We must develop metrics, some of which might involve testing, and some of which might not, to figure out how we are doing at our fundamental job of teaching. Any thoughts on such potential metrics are welcome.

Although the prominent critics of undergraduate education may have an imperfect grasp of history, nothing that has been said proves that colleges are above reproach. It may well be that undergraduate education has not suffered any discernible decline in quality over the past 50 or 100 years. But is that really a satisfactory outcome? Most human enterprise improves with time and experience. That is certainly true of consumer goods, athletic performances, health care, the effectiveness of our armed forces, the speed of our transportation and communication systems, and much else. Given the vastly expanded resources colleges have acquired, thanks to growing private donations, steadily rising tuitions, and massive infusions of federal financial aid, isn't it fair to expect the quality of education to improve as well?As we ask our students and their parents to invest more and more in higher education, we must do a better job of assessing learning. We as faculty can do this in part by giving more feedback to students; in the course of providing the feedback, we get to know better what our students know and what they don't. This has implications for how we structure instruction, about class sizes, about the use of TAs, and many other aspects of our teaching.To be sure, the undergraduate enterprise has grown in several dimensions. Millions more students enter college today than half a century ago. Countless new buildings have been built; faculties have greatly increased in numbers; new courses of every kind fill college catalogues to overflowing. Undergraduates can now watch PowerPoint lectures, print out articles at their personal computers, and receive homework assignments via the Internet. But all these changes, however broad in scope, say very little about what is truly important. Has the quality of teaching improved? More important, are students learning more than they did in 1950? Can they write with greater style and grace? Do they speak foreign languages more fluently, read a text with greater comprehension, or analyze problems more rigorously?

The honest answer to these questions is that we do not know. In fact, we do not even have an informed guess that can command general agreement.

But this is not enough. We must develop metrics, some of which might involve testing, and some of which might not, to figure out how we are doing at our fundamental job of teaching. Any thoughts on such potential metrics are welcome.

Greenstreet Advisors' Panel on Real Estate Markets

There is a good discussion at http://www.greenstreetadvisors.com/RE_portfolio.html.

The key takeaway is that one can be bullish on Texas and Arizona as economies without being bullish on their real estate markets. Because there places have few physical or legal restrictions on development, it is just about impossible to get real land price appreciation. The reason--as soon as real estate prices rise beyond construction costs, developers will build until prices are bid back down again.

Moreover, cities in Texas and Arizona generally have flat density gradients. They were built around the automobile; as such, no one part of Phoenix or Dallas is generally any more valuable than another. There are few exceptions--the Park Cities, two small towns that are surrounded Dallas, have exceptional school and can't expand, so the value of their schools gets capitalized into land prices. And Scottsdale's natural location makes it sufficiently unusual to get a price premium. But by and large, one subdivision in most sun-belt cities is pretty much like another, and so in the absence of constraints, the opportunity for price appreciation is limited.

The key takeaway is that one can be bullish on Texas and Arizona as economies without being bullish on their real estate markets. Because there places have few physical or legal restrictions on development, it is just about impossible to get real land price appreciation. The reason--as soon as real estate prices rise beyond construction costs, developers will build until prices are bid back down again.

Moreover, cities in Texas and Arizona generally have flat density gradients. They were built around the automobile; as such, no one part of Phoenix or Dallas is generally any more valuable than another. There are few exceptions--the Park Cities, two small towns that are surrounded Dallas, have exceptional school and can't expand, so the value of their schools gets capitalized into land prices. And Scottsdale's natural location makes it sufficiently unusual to get a price premium. But by and large, one subdivision in most sun-belt cities is pretty much like another, and so in the absence of constraints, the opportunity for price appreciation is limited.

Tuesday, August 29, 2006

Will the Housing Slump create a recession?

NYU Professor and Guru Noriel Roubini is arguing that it will--that the housing market is about to crash (especially in coastal cities, although not in Washington, D.C.), and that the crash will lead to a recession.

Housing is manifestly cooling off; housing is also a far more powerful leading indicator of the business cycle than business investment (see my 1997 paper in Real Estate Economics for the scoop on this. Email me if you want a copy).

But my model says it hasn't cooled off enough yet to produce a recession (despite what I told my colleagues the morning--oops). According to NIPA, seasonally adjusted residential invesment is off 6.3 percent in the second quarter, and was off a total of 1.2 percent in the previous two quarters. This should shave about .6 percent off of GDP; not a nice number, but not enough in and of itself to create a recession. If housing continues to get worse (and anecdotes suggest that it might), we could well get a recession by the second quarter of next year. I will wait for the third quarter residential investment numbers to come out before saying more.

Housing is manifestly cooling off; housing is also a far more powerful leading indicator of the business cycle than business investment (see my 1997 paper in Real Estate Economics for the scoop on this. Email me if you want a copy).

But my model says it hasn't cooled off enough yet to produce a recession (despite what I told my colleagues the morning--oops). According to NIPA, seasonally adjusted residential invesment is off 6.3 percent in the second quarter, and was off a total of 1.2 percent in the previous two quarters. This should shave about .6 percent off of GDP; not a nice number, but not enough in and of itself to create a recession. If housing continues to get worse (and anecdotes suggest that it might), we could well get a recession by the second quarter of next year. I will wait for the third quarter residential investment numbers to come out before saying more.

Where most affordable housing comes from--Old Houses

Sarah Kunkleman, who is Assistant Director for Communications in my school, asked me a good question today: if New Orleans were rebuilt, where would the affordable housing come from? After all, isn't old, dilapidated housing the cheap housing?

Sarah's insight is correct. A New York Times article from March 6 of this year describes work by Glaeser and Gyourko:

Indeed, old affordable housing almost certainly kept New Orleans'population from declining more rapidly than it did. The Glaeser-Gyourko work actually is part of a long tradition of urban economics work on "filtering." Ed Olsen at the University of Virginia wrote a paper in the early 1970s called "A Competitive Theory of the Housing Market," that predicted that in general the poor would live in the center of cities, for the simple reason that they would live where the old housing was. The poor actually tend to pay more for land rent than higher income people do, because (1) they can't afford to pay for transportation, and thus need to live near jobs and services and (2) because the old housing is on the most valuable (centrally located) real estate (it doesn't look valuable because the housing stock is so poor).

This phenomenon also explains why New Orleans population will likely not return to anything like what it was a little over a year ago. The "affordable" housing cannot be replicated, and so a principal reason many people stayed in New Orleans is gone forever.

Sarah's insight is correct. A New York Times article from March 6 of this year describes work by Glaeser and Gyourko:

"In 2000, Glaeser took a sabbatical from Harvard and began to spend a few days a week in Philadelphia working with Joseph Gyourko, a real-estate economist at the Wharton School of the University of Pennsylvania. Glaeser had already been thinking about the relationship between housing and urban poverty when one day he and Gyourko began to discuss why cities like Philadelphia and Detroit — places with poor future prospects, both economists believed — weren't doing even worse in terms of population. Why didn't everyone leave, Gyourko wondered, and go to a place like Charlotte, N.C., that had a fast-growing economy? This question addresses a puzzle of urban economics. Cities (think of Las Vegas or Phoenix) can grow at a very fast rate, exploding overnight with businesses and residents. Some can increase in population by 50 or even 60 percent in a decade. But cities lose their residents very slowly and almost never at a pace of more than 10 percent in a decade. What's more, when cities grow, they expand significantly in population, but housing prices tend to rise slowly; even as Las Vegas grew by leaps and bounds in the 1990's, for instance, the average home there cost well under $200,000. When cities decline, however, the trends get flipped around. Population diminishes slowly, but housing prices tend to drop markedly.

Glaeser and Gyourko determined that the durable nature of housing itself explains this phenomenon. People can flee, but houses can take a century or more to finally fall to pieces. "These places still exist," Glaeser says of Detroit and St. Louis, "because the housing is permanent. And if you want to understand why they're poor, it's actually also in part because the housing is permanent." For Glaeser, this is the story not only of these two places but also of Buffalo, Baltimore, Cleveland, Philadelphia and Pittsburgh — the powerhouse cities of America in 1950 that consistently and inexorably lost population over the next 50 years. It is not just that there were poor people and the jobs left and the poor people were stuck there. "Thousands of poor come to Detroit each year and live in places that are cheaper than any other place to live in part because they've got durable housing still around," Glaeser says. The net population of Detroit usually decreases each year, in other words, but the city still attracts plenty of people drawn by its extreme affordability. As Gyourko points out, in the year 2000 the median house price in Philadelphia was $59,700; in Detroit, it was $63,600. Those prices are well below the actual construction costs of the homes. "To build them new, it would cost at least $80,000," Gyourko says, "so there's no builder who would build those today. And as long as those houses remain, the people remain."

The resulting paper, "Urban Decline and Durable Housing," caused a stir among urban economists even before its publication last year. (It was initially circulated with a subtitle along the lines of "Why Does Anyone Still Live in Detroit?" until the authors, thinking it politically insensitive, removed it.) In addition to illuminating some of the forces shaping our poorest cities, the research proved to Glaeser that it is impossible to think about urban economies without thinking of urban buildings at the same time. "

Indeed, old affordable housing almost certainly kept New Orleans'population from declining more rapidly than it did. The Glaeser-Gyourko work actually is part of a long tradition of urban economics work on "filtering." Ed Olsen at the University of Virginia wrote a paper in the early 1970s called "A Competitive Theory of the Housing Market," that predicted that in general the poor would live in the center of cities, for the simple reason that they would live where the old housing was. The poor actually tend to pay more for land rent than higher income people do, because (1) they can't afford to pay for transportation, and thus need to live near jobs and services and (2) because the old housing is on the most valuable (centrally located) real estate (it doesn't look valuable because the housing stock is so poor).

This phenomenon also explains why New Orleans population will likely not return to anything like what it was a little over a year ago. The "affordable" housing cannot be replicated, and so a principal reason many people stayed in New Orleans is gone forever.

Urban Sprawl (Part 2)

Reasons 5 through 9:

V. GOVERNMENT SERVICES

Economist Charles Tiebout pioneered the idea that local units of government compete with each other for citizens. Specifically, he argued that local officials put forward packages of services in return for a given tax level, in the hope of attracting people and capital to their communities. This theory is supported by empirical evidence suggesting that people respond to service packages. Although it is often suggested that people seek to avoid taxes at all costs, work by Therese McGwire, Michael Wayselenko, and others has shown that people do prefer communities with better services, and tend to move to cities that provide the services they want at the lowest possible tax costs.

This competition puts newer cities at an advantage relative to their older counterparts. First, old cities’ infrastructures tend to be old and often inadequate, and replacing infrastructure is very expensive. Newer cities can offer better infrastructure at lower cost. Second, and perhaps more importantly, newer cities have often used land regulation to prevent the construction of low-priced housing. Old cities, on the other hand, have large amounts of old (low-priced) housing, which tends to attract low-income owners and tenants. Low-income people, who require a disproportionately large share of public services, are therefore concentrated in central cities. This concentration of individuals drawing on public resources puts central cities at a fiscal disadvantage as they try to offer “middle-class” benefits.

Newer cities, on the other hand, can provide these services at lower levels of taxes. Lower taxes attract the middle class, a migration that further increases the concentration of poverty in the older cities, which in turn worsens the older cities’ competitive position. Edward Glaeser argues that, because of this middle class exodus, higher levels of government (perhaps the federal government) should take responsibility for income redistribution and social services spending if older central cities are ever to become more competitive.

To make matters worse, older cities have often been run by politicians who are overtly hostile to private development in their jurisdictions’ central areas. This hostility stands in contrast to newer cities, which provide low tax rates on industrial parks and use tax-increment financing (TIF) to stimulate business development. Older cities are already at a fiscal disadvantage relative their less aged counterparts. But when the political class that runs an older city erects hoops (such as “pay-to-play” in Philadelphia) through which businesses must jump before they are allowed to develop, the fiscal disadvantages of the community grow even larger and harm the city and its residents.

VI. RACIAL DISCRIMINATION

Racial discrimination remains a central fact in U.S. housing markets; the statistical evidence, while in itself not conclusive, is nevertheless overwhelming. Leaving aside, for the moment, the moral repugnance of discrimination, discriminatory behavior is harmful because it generates perverse incentives, thus producing economically unappealing outcomes. One unwanted outcome is unnecessary sprawl. For example, “white flight,” by definition, requires development of land that would not be developed absent race related behavior. And while discrimination may have become a less pervasive element of individual minority group members’ treatment in the housing arena, the rising share of minorities in American society means that discrimination could become an increasingly destructive feature of the housing market in the years to come.

Consequently, one of the most important things that governments wishing to attack sprawl can do is to vigilantly and strictly enforce fair housing laws. After more than 30 years of federal fair housing laws, we still observe widespread patterns of discrimination and segregation, as numerous credible studies have shown. As time passes, it becomes clearer that testing is likely the only effective mechanism for enforcement. Testing involves sending equally financially qualified white and minority buyers and tenants into the housing market, and determining whether they are disparately treated. Disparate treatment implies discrimination, and thus is illegal. Putting widespread testing into practice is a severe and expensive means of enforcing fair housing laws, but if we, as a society, are serious about eliminating the blot of housing discrimination, we must do something serious in response.

VII. HOLDOUTS AND LAND ASSEMBLY

From at least one perspective, redeveloping at the city center always has a disadvantage relative to new development at the urban periphery: the cost of land assembly. Suppose that a company is considering where to locate a new manufacturing facility. If it can get zoning approval from the local government to develop at the periphery, then the company can negotiate an option to purchase from one landowner, typically a farmer. If the farmer will not sell at a price that is agreeable, then the developer of the facility can find another place to locate. By contrast, city centers tend to be characterized by any small parcels owned by different people. As a result, the owners of the last few parcels needed by a developer have monopoly power in setting price. Once the developer has bought the majority of parcels she needs, she may not be in a position to walk away from outrageous asking prices sought by a few holdout owners whose land is needed for the assembly to be complete. The periphery has another substantial advantage over the central city: property on the periphery is generally environmentally “clean,” while central city parcels often require costly environmental cleanups.

VIII. FEDERAL INCOME TAX POLICY

Federal tax policy has generally favored development on the periphery of cities. A striking example is the mortgage loan interest deduction (MID), which lets a household deduct home loan interest from ordinary income in determining its federal income tax liability. The MID is a residual part of the original tax laws; it was not designed to stimulate housing: the original 1913 federal income tax code allowed for deducting all consumer interest. It was the Tax Reform Act of 1986 that phased out consumer interest deductions, with one prominent exception: interest on a home mortgage loan. [Ed note: Add note here to update the state of MID.]

Yet the MID has done little to promote home ownership. The reason is that for those at the margin of home owning, the MID is not worth very much. Someone who pays little in property and state income tax might find that, even with the MID, the standard deduction is more valuable than itemization. Even for those who itemize, the MID can have little value, because the typical marginal federal income tax rate for low to moderate income families is 10 percent: each dollar paid in home mortgage loan interest is worth a mere 10 cents in tax relief. Contrast this situation with that faced by those higher up the income scale, where each dollar of deduction is worth between 25 cents and 45 cents, depending on the marginal tax rate. Of course, households with higher incomes are likely to own their homes regardless of the tax treatment of mortgage loan interest. Note that in Canada and Australia, countries without mortgage loan interest deductions, home ownership rates are quite similar to the rate in the United States.

On the other hand, the MID encourages high-income households to buy more expensive homes than they otherwise would, because the size of the implicit subsidy increases for costlier residences, up to a point (interest can be deducted only on up to $1.1 million of home loan debt). More expensive houses generally sit on larger lots than do less expensive homes. The tax code’s encouragement for buying relatively expensive houses therefore contributes to sprawl.

The tax treatment of parking had a more subtle effect. A firm on the Chicago periphery, where land was relatively cheap, could pave some acreage and provide free parking for its employees, a benefit on which users pay no income tax. Workers in the Loop, on the other hand, typically paid to park, a cost the IRS viewed as personal and therefore not deductible. (Parking in major downtown areas is uniformly expensive since the opportunity cost of land is too high to allow workers to park cheaply.) All things being equal, the suburban employee is better off. The implication was that the tax treatment of parking gives firms incentives to locate on the periphery, where land is cheap, rather than in city centers. This incentive was largely neutralized with the Tax Act of 1998, which went into effect in 1999.

IX. LAND USE REGULATION

I have already discussed how newer communities use land use regulation to prevent settlement by low income households, and how this activity contributes to sprawl. But even seemingly innocuous land use regulations can cause more land to be used than is necessary to house a given number of people. These regulations fall into a variety of categories, including setback, minimum lot size, street width, and, ironically, green space requirements. Simply put, all of these policies reduce the number of housing units that can be placed within a particular land area, in turn reducing population density, which, perforce, creates sprawl. World Bank planner Alain Bertaud has shown how seemingly small changes in these regulations can have a large impact on the number of housing units that can be fit into a particular land mass.

CONCLUSION

Sprawl has a variety of causes, some benign and others malignant. If policy makers are truly concerned about the malignant underpinnings of sprawl—discrimination, fiscal zoning, transportation that imposes social costs, federal tax policy, and regulations that needlessly consume land for residential development—then they will deal with these causes directly. Otherwise, we will know that they, and their voting constituents, are content with the way things are.

V. GOVERNMENT SERVICES

Economist Charles Tiebout pioneered the idea that local units of government compete with each other for citizens. Specifically, he argued that local officials put forward packages of services in return for a given tax level, in the hope of attracting people and capital to their communities. This theory is supported by empirical evidence suggesting that people respond to service packages. Although it is often suggested that people seek to avoid taxes at all costs, work by Therese McGwire, Michael Wayselenko, and others has shown that people do prefer communities with better services, and tend to move to cities that provide the services they want at the lowest possible tax costs.

This competition puts newer cities at an advantage relative to their older counterparts. First, old cities’ infrastructures tend to be old and often inadequate, and replacing infrastructure is very expensive. Newer cities can offer better infrastructure at lower cost. Second, and perhaps more importantly, newer cities have often used land regulation to prevent the construction of low-priced housing. Old cities, on the other hand, have large amounts of old (low-priced) housing, which tends to attract low-income owners and tenants. Low-income people, who require a disproportionately large share of public services, are therefore concentrated in central cities. This concentration of individuals drawing on public resources puts central cities at a fiscal disadvantage as they try to offer “middle-class” benefits.

Newer cities, on the other hand, can provide these services at lower levels of taxes. Lower taxes attract the middle class, a migration that further increases the concentration of poverty in the older cities, which in turn worsens the older cities’ competitive position. Edward Glaeser argues that, because of this middle class exodus, higher levels of government (perhaps the federal government) should take responsibility for income redistribution and social services spending if older central cities are ever to become more competitive.